In the ever-evolving landscape of the Greater Toronto Area (GTA) real estate market, the impact of the high mortgage rates, inflation, and the uncertainty surrounding the future Bank of Canada rate hikes continues to influence buyer bahaviour and market dynamics. As we delve into the latest market trends, it’s evident that significant shifts have occurred since the first couple of months of 2022.

Market Normalization:

The real estate market has undergone a process of normalization, steering away from the historical records set in 2021 and early 2022. The unsustainable trend of aggressive bidding wars during this period has given way to a more balanced market. The unprecedented 121,712 properties sold in 2021, a result of pent-up demand from the COVID-19 hit of 2020, set the stage for a recalibration.

Impact of Bank of Canada Rate Hikes:

With the increase of interest rate hikes by the Bank of Canada, the market began to normalize further. Prospective buyers, mindful of the changing economic landscape, shifted to the rental market. This shift resulted in an intense rental market, witnessed by soaring rents and bidding wars for available rental properties. , a more immediate comparison to June 2023 reveals a 29.8% decline, hinting at a market in transition. New listings, on the other hand, surged by 11.5% compared to July 2022 but faced a 13.5% dip compared to June 2023.

Stability in the Face of Uncertainty:

Contrary to concerns about a housing market crash, several factors suggest stability in the GTA. Aggressive population growth in Ontario, with over $1M in new residents added to Canada in 2022, places substantial demand on housing. The federal government’s commitment to increasing immigration and population growth exacerbates this pressure. The ongoing wealth transfer among baby boomers, and the early transfer of inheritances, further support the younger generation’s entry into the housing market.

Bank of Canada’s Rate Pause and Impact:

The Bank of Canada’s spring communication of possibly pausing interest rate hikes hinted at a cautious approach to assess the impact on inflation. This spring communication alluding to a possible pause prompted a temporary resurgence in buyer activity, particularly for smaller starter homes, however, the subsequent resumption of rate hikes in June and July led to a renewed retreat of buyers to the sidelines.

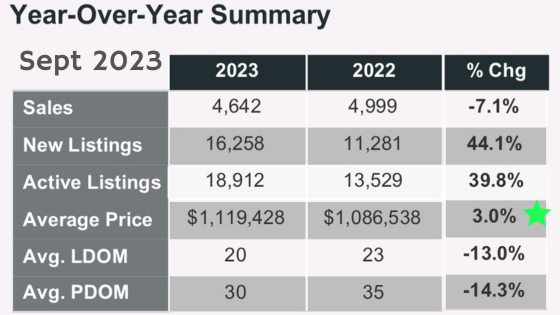

September Market Update:

September 2023 marked an unexpected downturn, with the lowest number of sales since the financial crisis of 2007/2008.

Uncertainty regarding interest rates prompted buyers to delay their home purchases. As we entered the fall market, sales typically picked up, but this year witnessed a notable increase in new property listings. The impact of reduced sales and increased listing inventory typically results in a drop in average sale prices. However, prices are up 3.4% compared to August 2023 and up 3% compared to September 2022. Historically the prices drop but what we are seeing alludes to the ongoing pressure on prices as we move forward.

Advice for Buyers and Investors:

Amidst this evolving market, our advice to first-time buyers, investors, and those eyeing recreational properties is clear: now is the time to act. Ontario’s appeal to high-profile employers ensures a sustained influx of new residents, contributing to the ongoing housing crisis. Developers struggle to match the pace of demand, emphasizing the urgency for buyers to enter the market. It all comes down to supply and demand and the supply of new housing stock is just not able to keep up with the demand and as a result, we will continue to see upward pressure on prices.

While uncertainties linger, we do not foresee a housing market crash in the foreseeable future. Waiting for the market to hit bottom is risky, as evident by the recent shifts. If you have questions or would like to chat, reach out. Let’s navigate this dynamic real estate landscape together.